Term Life Insurance and Its Investment Value

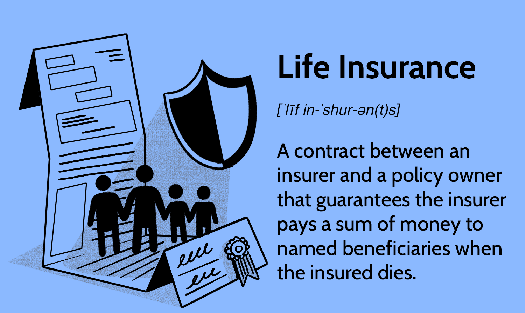

Value of Term life insurance is a financial instrument designed primarily to offer death benefits for a specified term, making it an essential component of risk management and financial planning. Unlike permanent life insurance, it does not accumulate cash value, which often leads to misconceptions about its investment potential. However, its affordability compared to cash-value policies makes term life insurance attractive for individuals seeking to ensure financial protection for dependents without the high costs associated with permanent options. This type of insurance serves as a foundational element in a comprehensive financial strategy, as it can free up resources for other investments, thus enhancing overall portfolio returns. As illustrated in , the direct nature of term life insurance contracts allows policyholders to focus their financial resources effectively, making it a viable tool for those prioritizing both immediate coverage and long-term investment growth.

II. Understanding the Mechanics of Term Life Insurance

When exploring the mechanics of term life insurance, it is essential to recognize how this financial product works to provide protection for policyholders beneficiaries. Term life insurance operates under a straightforward premise: the policy guarantees a death benefit for a specified term, typically ranging from one to thirty years, in exchange for regular premium payments. This structure is designed to offer financial security during critical life stages, yet it lacks a cash value component, unlike whole life insurance. Thus, the focus remains on providing a pure death benefit without additional savings elements, which can be appealing for those seeking affordability and simplicity in financial planning. As outlined in the mind map of personal financial management, highlighted in the image titled Financial Plan for the Suarez Family , understanding the role of term life insurance within a broader financial strategy can significantly enhance ones ability to ensure adequate safety nets for their loved ones while maintaining fiscal responsibility.

III. Evaluating the Financial Benefits of Term Life Insurance

A thorough assessment of the financial benefits of term life insurance reveals its significant role in a balanced investment portfolio. Unlike other investment vehicles, term life insurance provides a straightforward death benefit that can alleviate the financial burden on beneficiaries, thereby serving as a safety net for families. Additionally, its affordability relative to whole life policies makes it an appealing option for individuals looking to maximize their immediate financial security without the long-term commitment of accumulating cash value. This financial mechanism aligns with broader investment strategies, particularly in terms of risk management and asset allocation, which is crucial for maintaining a healthy financial outlook. Consequently, term life insurance can be integrated into existing financial plans to ensure not only life coverage but also a foundation for future investment endeavors, as illustrated in visual aids like , which showcase the policys core components and benefits. Moreover, insights from (ARFINTO et al.) and (Maurer et al.) underscore the strategic positioning of insurance products within overall financial health evaluations.

IV. Comparing Term Life Insurance to Other Investment Options

In evaluating the merits of term life insurance against alternative investment options, it is crucial to consider its unique advantages, particularly regarding risk management. Unlike traditional investments that expose individuals to market fluctuations, term life insurance offers predictable financial protection during critical life stages, effectively mitigating longevity risk, investment risk, and unexpected events such as medical emergencies (Mulvey et al.). The security it provides allows policyholders peace of mind, which is often absent in volatile investments. Moreover, as individuals approach retirement—when the necessity for reliable income streams becomes paramount—decumulation strategies, which encompass the withdrawal of funds from retirement accounts, become especially pertinent (Rashbrooke G). Hence, while investments like stocks or bonds may offer potential growth, they do not inherently provide the same level of guaranteed financial support for dependents in the face of unforeseen circumstances, emphasizing the complementary role of term life insurance in a robust financial strategy. The mind map in succinctly illustrates how term life insurance integrates with various financial planning components, reinforcing its value as an investment.

V. Conclusion

In conclusion, assessing the value of term life insurance as an investment reveals its dual role as both a financial safeguard and a strategic asset for long-term planning. While it primarily functions to provide financial security for dependents in the event of premature death, its affordability and straightforward nature make it an attractive option for individuals seeking to enhance their overall financial health. Additionally, as illustrated in , the essence of life insurance is rooted in planning for the future, effectively conveying the necessity of evaluating personal circumstances when making such investments. Ultimately, term life insurance not only serves as a protective measure but also encourages policyholders to engage in broader financial planning strategies, ensuring they cater to their present needs while securing a safety net for their loved ones. This multifaceted perspective underscores its importance in a comprehensive financial strategy.

References:

- ARFINTO, Erman Denny, PRIMAYANTI, Asih. “THE DETERMINANT OF FINANCIAL HEALTH ON SHARIA LIFE INSURANCE COMPANY (Empirical Research on Sharia Life Insurance Company in Indonesia Period 2010-2015)”. 2016, https://core.ac.uk/download/76934519.pdf

- Maurer, Raimond. “Institutional investors in Germany : insurance companies and investment funds”. 2003, https://core.ac.uk/download/14503633.pdf

- Mouthaan, A.J., Vegt, J.J.W. van der. “Self-Evaluation Applied Mathematics 2003-2008 University of Twente”. Faculty of Electrical Engineering, Mathematics and Computer Science, University of Twente, 2009, https://core.ac.uk/download/pdf/11473171.pdf

- Aditi Mehta, Charlotte B. Kahn, Jessica K. Martin. “City of Ideas: Reinventing Boston’s Innovation Economy: The Boston Indicators Report 2012”. The Boston Foundation, 2012, https://core.ac.uk/download/71357865.pdf

- Mulvey, Janemarie, Purcell, Patrick. “Converting Retirement Savings into Income: Annuities and Periodic Withdrawals”. DigitalCommons@ILR, 2008, https://core.ac.uk/download/5131466.pdf

- Geoff Rashbrooke. “Decumulation 101: the basics of drawing down capital in retirement”. Institute for Governance and Policy Studies (VUW), 2014, https://core.ac.uk/download/pdf/30673936.pdf

Car Insurance: How to Guard Your Car and Your Pocket, Insurance: Financial Protection, Construction truck accident caught on camera, Top insurance plans to choose for term insurance, Understanding the basics of insurance a comprehensive guide, How to find top 10 truck accident insurance